Portfolio Update

Disclaimer: I am not your advisor. Nothing in this post is investment advice, financial advice, legal advice, or tax advice. This is purely my personal opinion. You are responsible for your own decisions, and you should do your own research and consult a qualified financial advisor. Your capital is at risk.

Performance

This week, the portfolio has shown an exceptional performance, driven by the resilience of the selected stocks, exceptionally strong market reaction on AXTI 0.00%↑ earnings report, and the tariff Supreme Court ruling tailwinds.

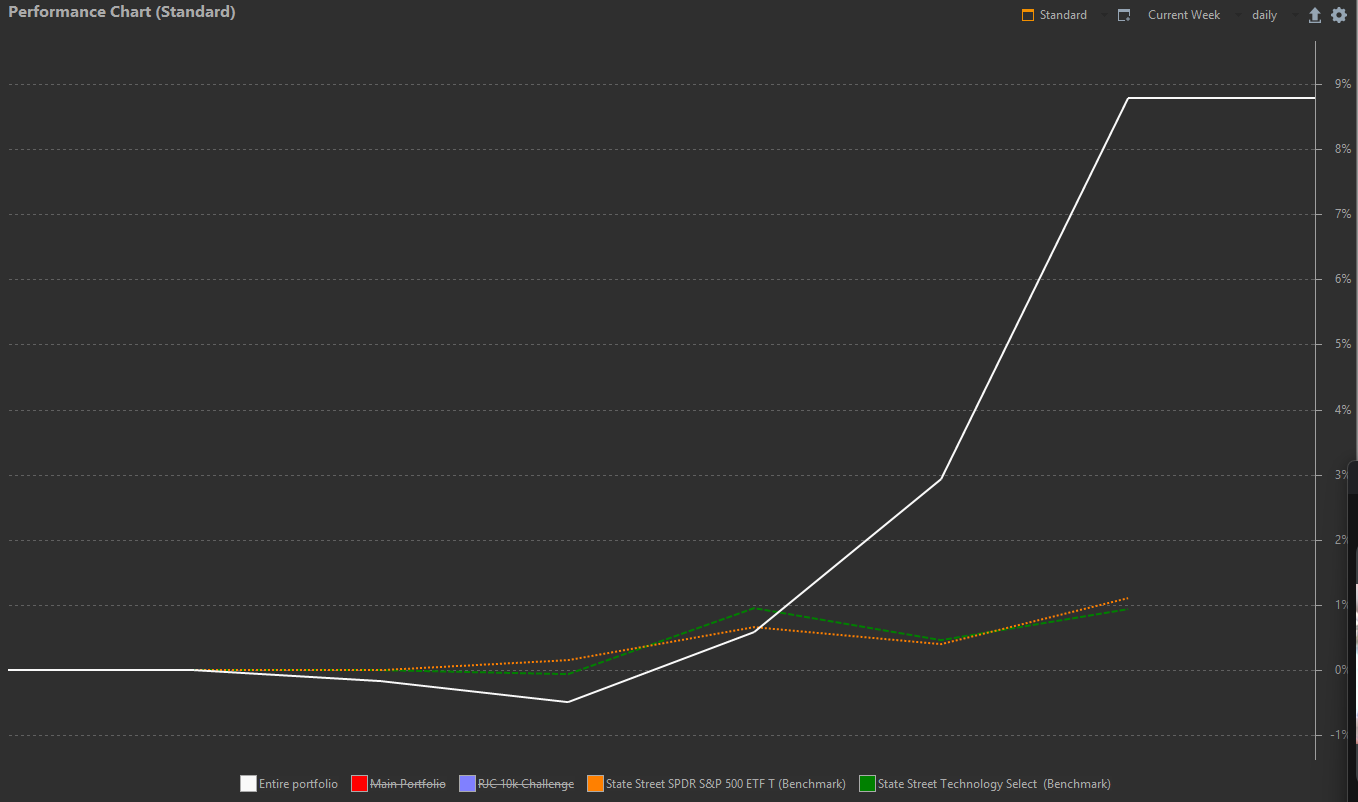

The entire portfolio’s TTWRoR yielded almost 9% over the week, whereas SPY 0.00%↑ and XLK 0.00%↑ just progressed 1%:

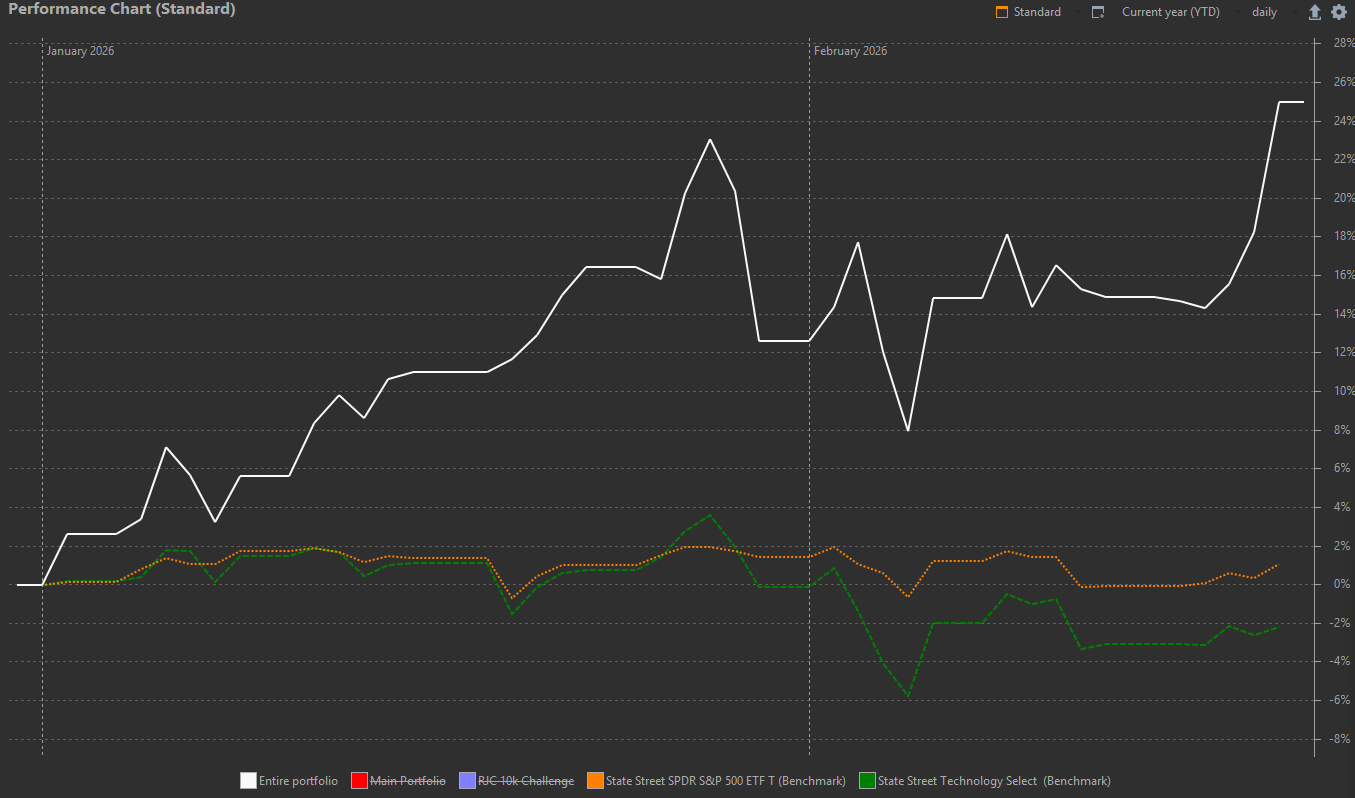

Year-to-date, the portfolio’s TTWRoR renewed the ATHs, ending 25% up, while the overall market stalled:

I am well on the roadmap to my self-imposed target to make 100% return in 1 year with the annualized rate over 300% thus far.

The entire portfolio is comprised of two parts: my own trades (~80% of funds) and RJC’s $10k challenge (the remaining 20%).

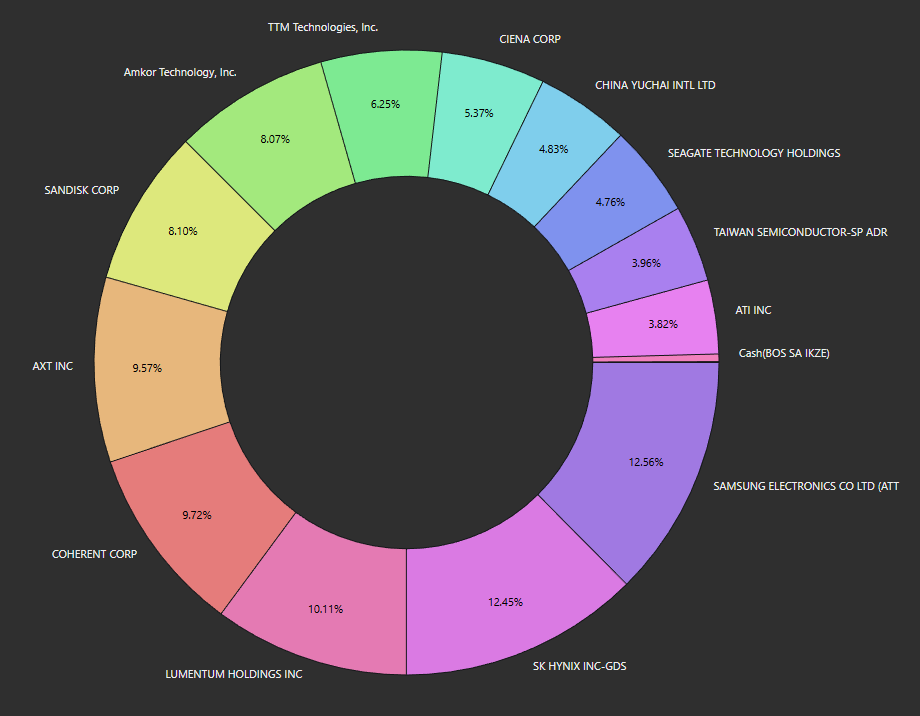

This is what the main portfolio looks like by the end of the week:

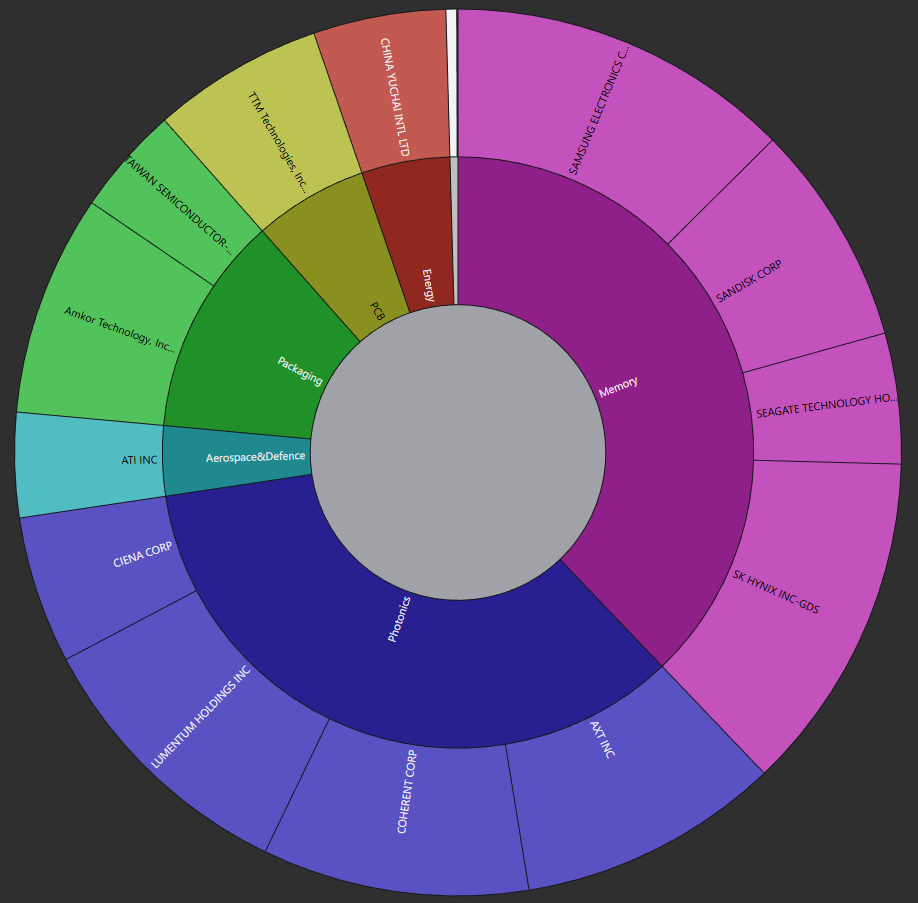

And this is the theme allocation distribution:

Trades

This week I’ve made two trades: I bought one share each of SNDK 0.00%↑ and Samsung. I maxxed out my IKZE (the Polish analog of IRA/RRSP) yearly contributions and wanted to balance off my position in SK Hynix withing the memory theme of my portfolio during the market retreat on Tuesday. Both ended up to be profitable trades (thus far). I am not particular proud of the SNDK 0.00%↑ purchase, because the more prudent approach would be to wait for the WDC 0.00%↑ debt-swap deal to go thru first, where they planned to sell SNDK 0.00%↑ to the financial instituitions at a significant discount. I let it slide, because the trade volume was miniscule both relative to the portfolio and the position sizes.

All-in-all, this week I avoided significant moves (partially, because I ran out of the commission-free limit at one of the brokers), and the portfolio did the job for me.

Review

I am very happy with the previous job I have done of aggressively culling smaller and low-conviction positions and consolidating money in a few high-conviction plays. The results have been visible immediately with the increduible run of photonics overall culminating with the AXTI 0.00%↑ incredible post-earnings. Let’s review every position held.

Memory

Samsung and SK Hynix: with the memory supercycle, they remain my highest conviction positions in the DRAM/HBM domain. They offer much better valuations than MU 0.00%↑ without a negative sentiment. They are also hugely underappreciated due to being unavailable thru the most popular platforms (HOOD 0.00%↑), but retail investors are gradually getting exposed to it thru EWY 0.00%↑.

SNDK 0.00%↑: my NAND (Flash) memory pick. The forward P/E is still ridiculously low (in the 1-digit zone), so despite being late to the party, it is still an underappreciated company producing a bottleneck commodity.

STX 0.00%↑: I am not convinced HDD are nearly as limited now as DRAM/HBM/NAND/NOR. I am planning on selling it early next month (to have my free limit renewed) and allocating cash to other themes. That would also bring memory to about 1/3 of my portfolio allocation, which I am extremely comfortable with.

Photonics

AXTI 0.00%↑: an extremely volatile, yet amazingly positioned company that has a hold of the InP substrate production (they are essentially a duopoly), being upstream from the rest of my photonics portfolio in the bottleneck flow. Their only problem is the Chinese export licenses, which should be resolved with tariff wars coming down, hopefully. Otherwise, their Chinese client market is rapidly growing, so they would sell inside what they can’t export. I am not happy with my entry point, being very close to the top ceiling curve, so that would be a good motivation to study more of technical analysis and avoid paying 15% premium for no reason.

LITE 0.00%↑: its run has been nothing short of amazing. What is more important though, is that they’ve shown a lot of resilience during early February during selloff times — that shows a high conviction of the investors getting margin calls, but holding onto it. They address a bottleneck of ALL of the hyperscalers, providing lasers for the co-packaged optics, among other things.

COHR 0.00%↑, CIEN 0.00%↑: other photonic plays that did exceedingly well. I am looking forward to getting to know CIEN 0.00%↑ better at their earnings call in early March.

Packaging

AMKR 0.00%↑: this is my play in the hybrid bonding. Again, highly volatile, and the wrong entry point costed me more than it should have.

TSM 0.00%↑: while being a huge cap and thus having a limited upside, they have an amazing exposure to multiple bottlenecks, including CoWoS and clean room space, needed for hybrid bonding. I consider upgrading this position to the full size (as well as upgrading exposure to the packaging theme).

Aerospace&Defense

ATI 0.00%↑: an interesting company, both decently profitable and valued (a rare combo for any defense stock), and sitting on the engine production bottlenecks.

Printed Circuit Board

TTMI 0.00%↑: the company is healthy and is having an amazing run, but I am not entirely sold on the moat and bottleneck of the PCB business. I will be keeping my eye on it and potentially allocating these funds elsewhere.

Energy

CYD 0.00%↑: one may think about it as a legacy business. But China Yuchai is increasingly building diesel and hydrogen engines (together with Rolls-Royce) for Chinese data centers (Bytedance being one of their clients). Their fundamentals look much healthier than most energy plays out there. I am looking forward to getting to know them better during an earnings call next week and considering updating them to a full position.

Positions I am considering

NBIS 0.00%↑ — a finX ‘misunderstood’ darling. I want to like them, but I’ll wait until they overcome a technical ceiling around $108. I am attracted to adding a datacentre buildout theme to my portfolio, and the team is amazing.

LASR 0.00%↑ — I really want to extend my exposure to the defense sector, and I really like this company at face value. I am looking forward to their call next week. My main concerns are the DEW's feasibility in the adverse atmospheric conditions and the poor outlook of their management.

GLW 0.00%↑ — moving from producing glass for iPhones to fiberglass and substrate has been an amazing pivot point.

FIX 0.00%↑ — they just had amazing Q4 results, and a datacenter buildout theme absent from my portfolio. I need to read up more on their moat and bottlenecks addressed.

Whoa, my first post got much longer than I originally anticipated! I hope it’s been insightful and informative for you. And what are the companies you’re looking at? What are your results? What do you want me to discuss next time? Don’t be a stranger and drop a comment.

As you are an active trader, it would be very interesting to read what indicators do you use mostly for your technical analysis.